SMM News on May 8:

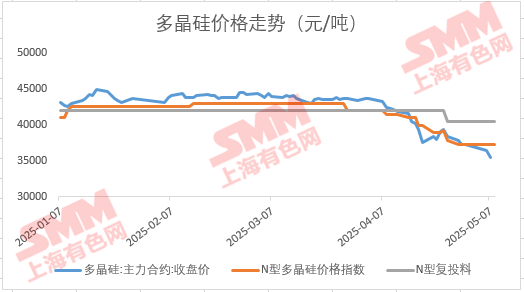

On May 8, the polysilicon futures market opened with another significant decline, with the lowest intra-day drop reaching 4% in the morning session. By the midday close, the most-traded PS06 futures contract returned to positive territory, closing at 36,295 yuan/mt. What are the reasons behind the weakness of the most-traded polysilicon futures contract after the Labour Day holiday? Is the current price reasonable compared to the spot market? What is the real supply-demand situation in the market?

According to SMM's market insights, the weakness in the polysilicon futures market is not only influenced by capital flows but also fundamentally driven by the previous price declines across the entire PV industry chain and the pessimistic outlook for demand following the "531" installation rush. The overall sentiment in the downstream sector remains pessimistic. Meanwhile, the continuous decline in wafer and solar cell prices has also exerted considerable downward pressure on spot polysilicon prices.

However, it is worth noting that with the recent weakness in the futures market, futures prices have gradually fallen below spot prices. According to SMM, the transaction price for N-type polysilicon in the market before the Labour Day holiday was around 37,000 yuan/mt. Subsequently, as market sentiment weakened, several polysilicon enterprises even withdrew their quotes and chose to suspend quoting. By May 8, the price of the most-traded PS06 futures contract had dropped to a low of 34,375 yuan/mt, creating a significant price spread with previous spot prices. Some downstream enterprises have even begun to calculate the feasibility of purchasing from the futures market.

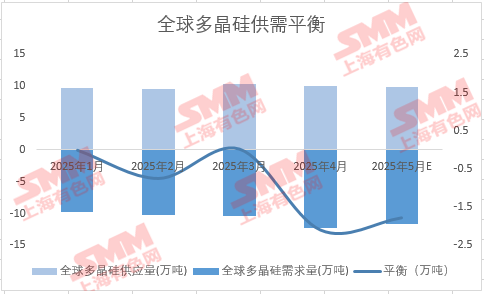

Regarding market supply and demand, according to SMM data, global polysilicon production in May is expected to be around 99,000 mt (including 94,500 mt of domestic production), representing a decrease of approximately 2% MoM from April. Although downstream wafer production has also declined MoM, global wafer production is expected to be around 57-58 GW, with wafer demand for polysilicon at approximately 110,000 mt. There may be some destocking expectations for polysilicon in May. Currently, the delivery brands held by many of the five enterprises are relatively limited (mostly concentrated in a few thousand mt). However, it cannot be denied that polysilicon enterprises have been facing some inventory pressure recently, and crystal pulling plants also have relatively abundant raw material inventories, which are the main reasons for the weakness in the polysilicon spot market at the end of Q1 and the early stage of Q2. This pressure is expected to be alleviated to some extent as the supply-demand relationship improves.

Regarding the future spot market, SMM has learned that some top-tier enterprises are gradually increasing their willingness to stand firm on quotes based on cost rationality. There are also plans to reconvene relevant industry meetings in the near future, and some production capacities are experiencing delayed resumption and commissioning, which may have a positive impact on the subsequent market. It is recommended to closely monitor the operational status of major production capacities and the price trends of downstream wafers.

》View SMM's PV Industry Chain Database

![[SMM PV News] Armenia Hits 1.1 GW Solar Capacity,](https://imgqn.smm.cn/usercenter/qQwIB20251217171741.jpg)

![Spot Market and Domestic Inventory Brief Review (February 5, 2026) [SMM Silver Market Weekly Review]](https://imgqn.smm.cn/usercenter/tSwaX20251217171735.jpg)